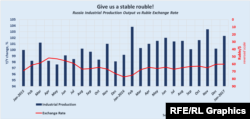

The exchange rate of the ruble to the dollar has increased 30 percent over the past 13 months, mainly as a result of the rising price of oil, Russia’s main export.

“The fact the ruble has risen, is rising, is definitely a negative for our exports,” stated Aleksandr Tkachev in a TV interview. “Not only for the agricultural sector, but for industry and many other sectors of the economy as well.”

The minister is partially right when referring to Russia’s agricultural sector.The stronger ruble, however, is only part of the reason for Russia’s falling agricultural export numbers, and not the main one. A huge surplus of grain stocks at home amid a general slump in global agricultural prices are the main culprits (see graphic).

In 2016, Russia’s grain harvest was the most bountiful in modern Russian history – more than 120 million tons. With domestic grain consumption calculated at between 72 to 74 million tons, Russia’s Ministry of Agriculture estimated grain exports for 2017 could reach 35 to 40 million tons.

The U.S. Department of Agriculture as late as August 2016 was predicting that in 2016/2017 Russia could become the world’s biggest wheat exporter (30 million tons – out of 170 million overall export figure), ahead of the EU (27 million) and the U.S. (some 26 million).

However, Russian grain exports for the period between July 2016 and February 2017 were 4.5 percent lower than for the same period a year earlier, including a 2 percent drop for wheat exports, noted Igor Pavenski, a deputy director at Rusagrotrans. And with importer demand tending to wane from March, Pavenski is not expecting any rebound in Russian grain exports this year.

Sluggish agricultural exports amid a record harvest inevitably led to a sharp rise in stored grain reserves in Russia. According to estimates by Rusagrotrans, such reserves hit an eight-year high in December 2016, and by the end of June 2017 could be double what they were last year.

And although these surplus stocks in Russia have not yet caused a drop in domestic grain prices, it may only be a question of time, especially by the spring when the attention of the agriculture market turns to the next harvest. And Russian agricultural output is expected to be strong again, albeit not as strong as in 2016.

But the main reason for the slowdown in Russian grain exports has been low global prices. For the past ten years, global grain output has outpaced demand, according to the UN’s Food and Agriculture Organization (FAO). As a result, grain surpluses have risen by 1.5 times, and the price of wheat, Russia’s main grain export (80 percent of the total) has dropped by 2.5 times over just the past five years.

And the FAO is predicting worldwide wheat production for the 2016/2017 season will again outpace global demand, meaning prices likely won’t be rising any time soon.

The dim prospects of profitability have put a brake on Russian grain exports. Moreover, Russian wheat exporters aren’t eager to sell their crop at reduced prices to companies and exporters, holding on to what they have in the hope of a future rise in the price of the commodity.

Given these circumstances, a stronger ruble merely becomes a secondary risk factor, as Tkachev pointed out.

For example, a small rise in the price of Russian wheat at the start of 2017 (some 4 percent) was offset by a further strengthening of the ruble (also 4 percent by the end of February). Therefore, even a small reduction in the value of the ruble at the start of March led to a rise in Russian grain exports and forecasts of greater global demand for the commodity.

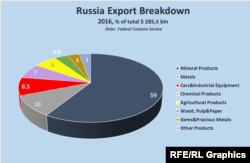

Grains exports will be kick-started if the ruble falls to at least 60 to the dollar, Arkady Zlochevski, president of the Russian Grain Union, forecast on February 28. By the middle of March, the ruble was trading at some 59 to the dollar. However, agricultural exports are just a sliver of Russia’s overall export pie, contributing only 6 percent. Oil, oil products, and natural gas remain king, accounting for nearly 60 percent of all Russian exports (see graphic). And this market has its one unique set of rules. In 2016, the price of oil, unlike grain, more than doubled. Oil drilling in Russia was up 2.5 percent in 2016, hitting another post-Soviet high, despite a robust ruble.

The ruble exchange rate impacts greatly on the Russian state budget, dependent as it is on income from the oil and gas sectors. However, the budget is calculated in rubles, and for the Ministry of Finance the “ruble” price of oil is of particular interest. And that price is not only dependent on the price of oil, but the exchange rate of the ruble as well. So, when the price of oil drops, the ruble follows as well, maintain the “ruble” price for oil in a comfortable range for fulfilling the government budget. But if amid relatively stable oil prices the ruble rises, then the “ruble” price of oil falls, creating certain budgetary risks.

Respectively, with “oil and gas” revenue now comprising 39 percent of the Russian state budget, every time the ruble rises by 5 percent the state budget takes a hit to the tune of about 2 percent, explained Aleksei Devyatov, the head economist at Russia’s Uralsib bank in an interview with RFE/RL’s Russian Service.

As a result, the federal government decided in 2017 to “insure” the federal budget against possible fluctuations in the global price of oil. The revenue for the budget is calculated based on a price for oil of $40 a barrel (the actual price of crude is about $ 51 now). For all “additional” oil and gas revenues (in rubles) arising when oil is selling above $40 a barrel, the Russian Ministry of Finance, beginning in February 2017, regularly and in moderate amounts, (1-3 percent of all daily currency trading on the Moscow Stock Exchange) began interceding in the currency markets buying dollars or euros to control the value of the ruble.

Nonetheless, the current year Russian federal budget has been calculated based on an average ruble exchange rate of 67.5 to the dollar. The current exchange rate is about 59 rubles. Some predictions of its further weakening in coming months (if the oil prices fall again) – is good news for Russia’s grain producers and the Ministry of Agriculture.

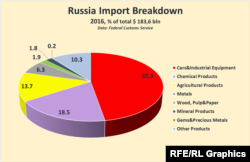

However, not so for much of Russia’s industrial sector. A glance at the breakdown of Russian imports (see graphic) shows that nearly half of the purchases of equipment and raw materials, needed for production.

So-called import substitution, which was all the buzz in the corridors of power in 2015, has proved a failure. Seventy percent of Russian industrial enterprises, based on interviews and surveys, need to maintain these industrial imports at previous levels.

The reason is simple: there are no equivalents in Russia, either in price or quality, for the equipment and raw materials imported from abroad.

And that’s why a “weak” ruble remains one of the biggest risk factors for Russian industrial enterprises, unlike for the country’s grain exporters.

Trying to figure out the “optimal” ruble rate for Russia industry is something the government and experts have attempted. In December 2016, Minister of Finance Anton Siluanov stated that for Russian industry, “which is already use to the exchange rate of 60 rubles for one dollar, further strengthening of the Russian currency would reduce their competitiveness.” Deputy Minister of Industry and Trade Vasily Osmakov noted on March 1 that surveys by his ministry indicated many in Russian industry considered an ideal ruble rate to the dollar somewhere in the band between 60-65.

Different experts give different estimates. So, the Gaidar Institute for Economic Policy, which has been conducting business surveys for over a quarter century, ran a poll in May 2016 commissioned by the Russian Central Bank on the ideal ruble exchange rate.

51 rubles to the dollar was the optimal rate that emerged from that survey (the exchange rate at the time was 65 rubles to the dollar). The institute took up the question again just weeks ago at the end of February, when the exchange rate was 57.5 rubles to the dollar. 54.8 was the average ideal rate to emerge from that polling of industrialists.

Although ruble rates may vary in such polls, what seems to unite them all is an apparent desire of many Russian industrial leaders: a “stable” ruble exchange rate.

So, while the value of the ruble is definitely a factor for both Russian industry and agriculture, a stable rate may be even more important.